Getting your motor insurance in the UAE isn’t just about protecting your wheels, it’s also about keeping your wallet in check. But how are those insurance rates determined?

In this article, we’ll take a closer look at the key factors that play a role in shaping the cost of motor insurance premiums in the United Arab Emirates. By understanding these factors, you’ll be better equipped to make informed decisions and potentially find ways to save on your coverage.

Defining Motor Insurance

This is your financial guardian, the safety net that shields you from the unexpected storms of vehicle-related costs. Whether it’s a fender-bender, a parking lot mishap, or a full-on collision, motor insurance is your steadfast companion.

Understanding Insurance Premiums: But, of course, every superhero needs support, and that’s where insurance premiums come into play. These are the regular payments you make to keep your coverage intact. However, buckle up because premiums are as diverse as the roads we travel, influenced by a multitude of factors.

Importance of Premiums: So, why should you care about these premiums? Well, imagine them as the tolls on your financial journey. The more you pay, the costlier your ride becomes. Understanding these costs is vital because it’s not just about driving; it’s about making informed choices to ensure your financial road trip stays smooth and affordable. Ready for the ride? Let’s dive into the intricate world of motor insurance.

Types of Motor Insurance in the UAE

In the UAE, when it comes to insuring your vehicle, you have several options to choose from. Each type of motor insurance offers different coverage levels and comes with its own price tag. Understanding these options is the first step in determining the cost of your motor insurance premium.

- Comprehensive Insurance: This is the most extensive and often the costliest type of motor insurance. It covers damages to your vehicle, liability towards third parties, and other potential expenses like theft and natural disasters.

- Third-Party Liability Insurance: This is the minimum legal requirement for any motorist in the UAE. It covers your liability towards third parties in the event of an accident. While it’s the cheapest option, it offers the least coverage for your own vehicle.

- Additional Coverage Options: In addition to these primary types, you can often choose from various add-ons and optional coverages, such as roadside assistance, agency repair, and personal accident coverage. These add-ons can customize your policy to better fit your needs, but they will also influence the overall premium.

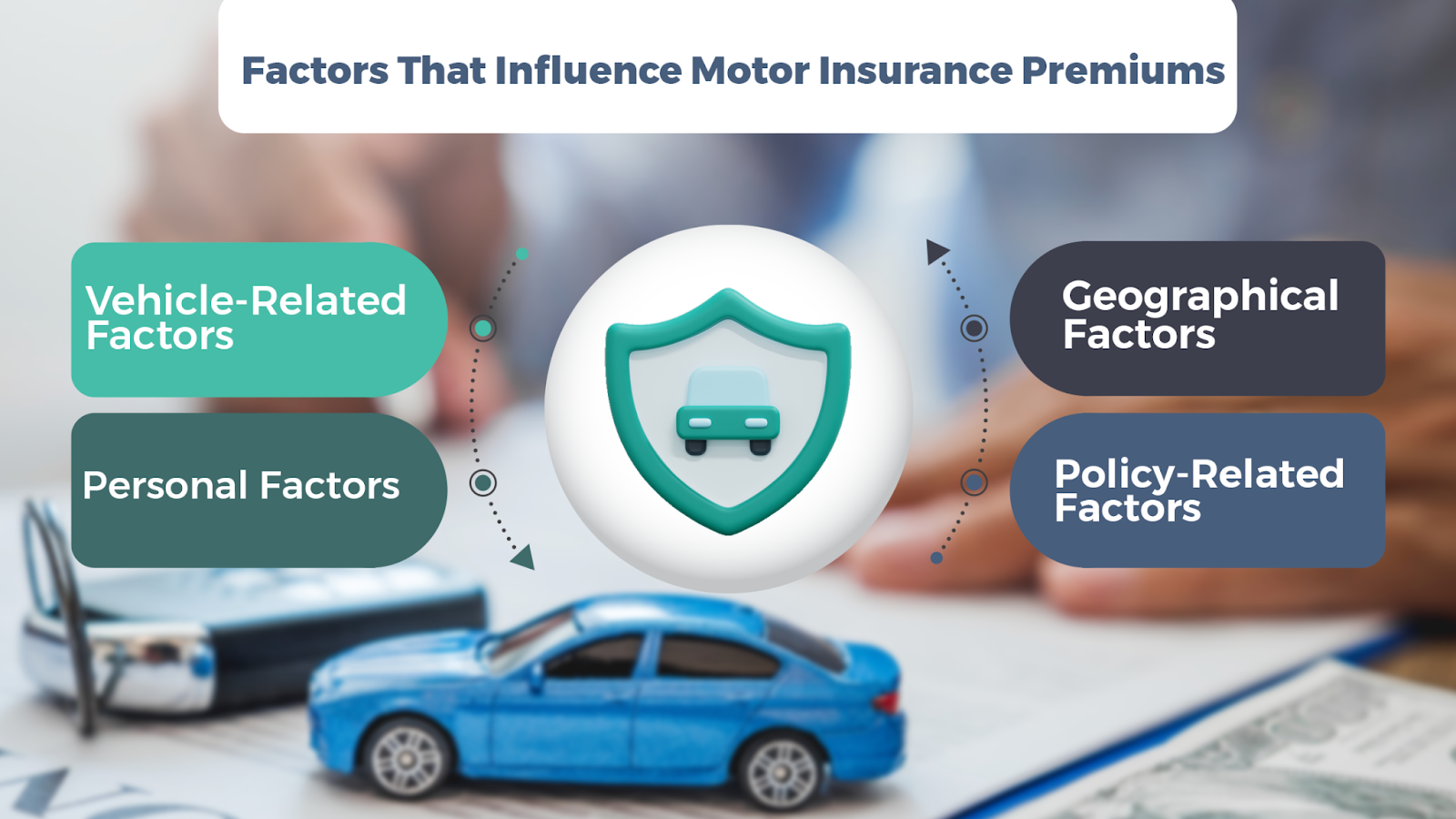

Factors That Influence Motor Insurance Premiums

The cost of motor insurance premiums in the UAE fluctuates based on a range of factors. These elements fall into a few important categories.

Vehicle-Related Factors:

- Vehicle Make and Model: The make and model of your car play a significant role in determining your premium. High-end and luxury vehicles often come with higher insurance costs due to their expensive repair and replacement parts.

- Age and Condition of the Vehicle: The age and condition of your vehicle can affect the premium. Older cars may have higher premiums, while brand-new cars might be more expensive to insure due to their high replacement value.

- Safety Features and Anti-Theft Devices: Vehicles equipped with advanced safety features, such as airbags, anti-lock brakes, and anti-theft systems, may qualify for discounts on their premiums.

Personal Factors:

- Age and Gender of the Driver: Young and inexperienced drivers typically face higher premiums due to the increased risk associated with their age group. Additionally, gender can also be a factor, as some insurers may consider males to be higher-risk drivers.

- Driving Experience and History: A clean driving record with no accidents or traffic violations can help lower your premium, while a history of accidents and violations can lead to higher costs.

- Occupation and Income: Some insurers take your occupation and income into account when calculating premiums, as certain professions may be associated with safer driving habits.

Geographical Factors:

- Location and Parking Situation: Where you live and where you park your vehicle can affect your premium. Higher premiums may result from urban locations with greater rates of traffic and crime.

- Theft and Accident Rates in the Area: Insurance companies consider the theft history and accident rates in your area, which can influence your premium.

Policy-Related Factors:

- Coverage Limits and Deductibles: The coverage limits you choose and the deductible amount you’re willing to pay out of pocket in the event of a claim can impact your premium.

- Additional Coverage Options: Adding optional coverage, such as personal injury protection or rental car coverage, will increase your premium.

- No-Claims Discount: Many insurers offer no-claims discounts for policyholders who have not made any claims in a specified period, which can lead to premium reductions.

Regulatory Factors in the UAE

In the United Arab Emirates, motor insurance is regulated by government authorities to ensure the fair and responsible operation of the insurance industry. These regulations have a direct impact on how motor insurance premiums are calculated and offered. Here are some key regulatory factors that influence the cost of motor insurance in the UAE:

- Mandatory Third-Party Liability Insurance: The UAE law mandates that every vehicle owner must have third-party liability insurance. This ensures that all road users have a minimum level of protection in the event of an accident. While this requirement may seem like it would lead to lower premiums, the cost is often influenced by other factors.

- No-Claims Discount (NCD): The UAE Insurance Authority has established guidelines for the no-claims discount system. Insurance companies offer reduced premiums to policyholders who have a claim-free history. The level of discount may vary among insurers, but the regulatory framework ensures a degree of consistency.

- Claims Processing and Dispute Resolution: The UAE has mechanisms in place for the fair processing of insurance claims and dispute resolution, ensuring that policyholders receive fair treatment in the event of a claim.

As a consumer, being aware of these factors can help you navigate the motor insurance market in the UAE more effectively.

Tips to Lower Motor Insurance Premiums

While motor insurance premiums are influenced by various factors, there are strategies and practices you can adopt to potentially reduce the cost of your coverage. Here are some valuable tips to help you save on your motor insurance premiums in the UAE:

A. Safe Driving Practices:

- Defensive Driving: Enroll in defensive driving courses to improve your driving skills and reduce the risk of accidents.

- Avoiding Traffic Violations: Abide by traffic laws and regulations to maintain a clean driving record, which often leads to lower premiums.

- Defensive Driving Courses: Policyholders who successfully complete defensive driving courses may be eligible for discounts from some insurers.

B. Vehicle and Security Measures:

- Installing Security Features: Equip your vehicle with anti-theft devices and safety features to reduce the risk of theft or accidents.

- Parking in a Secure Location: If possible, park your car in a secure location such as a garage or a well-lit area to lower the risk of theft and damage.

C. Comparison Shopping:

- Getting Quotes from Multiple Insurers: Don’t settle for the first insurance quote you receive. To discover the best bargain, shop around and get quotes from several insurance providers.

- Understanding the Policy Terms: Carefully read and compare the terms and conditions of different policies to ensure you’re getting the coverage you need at a competitive price.

D. Utilizing No-Claims Discount:

- Maintaining a Claim-Free Record: Avoid making small claims that can negatively impact your no-claims discount. Instead, save it for significant incidents.

- Transferring No-Claims Discount: If you change insurers, inquire about transferring your no-claims discount to your new policy.

Conclusion

In the UAE, understanding the factors influencing motor insurance premiums is vital for making smart and cost-effective choices. By considering your coverage, safe practices, and opportunities for savings, you can protect your vehicle and your budget. Make informed decisions, drive safely, and choose your coverage wisely for a secure and economical journey on the road.